Overview

Fixed costs:

A fixed cost is a cost that tends to be unaffected by increases or decreases in the volume of output.

No matter what a business does in any given month, it still has to pay salaried employees and the lease on its office space.

Some firms operate in a situation where the fixed cost represents a large proportion of the total. In this case, it would be wise to produce a large output in order to reduce unit costs and so make the firm more efficient.

Variable costs:

A variable cost is a cost that tends to vary directly with the volume of output.

If you're in the business of creating cotton T-shirts, the more T-shirts you produce, the more cotton fabric you'll need. Raw materials, usage-based utilities, and hourly workers are all variable costs.

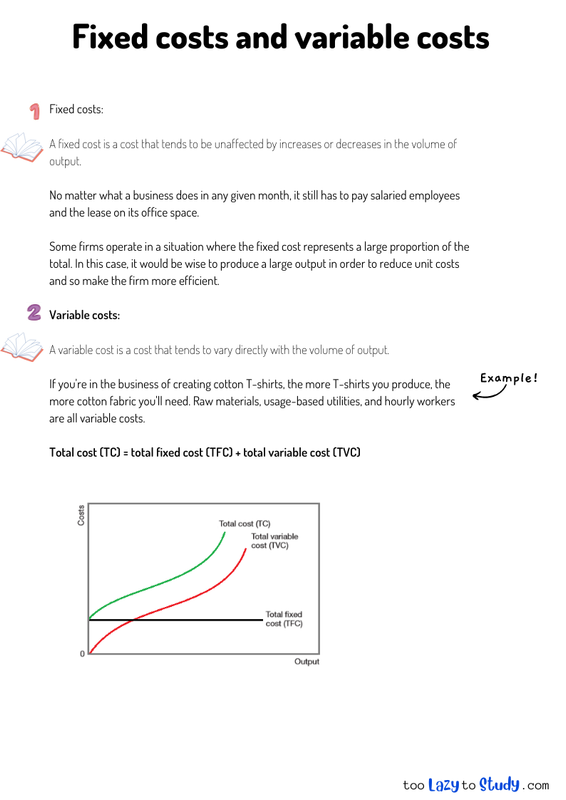

Total cost (TC) = total fixed cost (TFC) + total variable cost (TVC)

.png)

Economics notes on

Fixed costs and variable costs

Perfect for A level, GCSEs and O levels!