Overview

A maximum price is a price ceiling set by the government or some other agency. The price is not allowed to rise above this level.

Maximum price controls are only valid in markets where the maximum price imposed is below the normal equilibrium price as determined in a free market.

Example: Governments use legislation to enforce maximum prices for basic services provided by utilities, such as water, gas and electricity

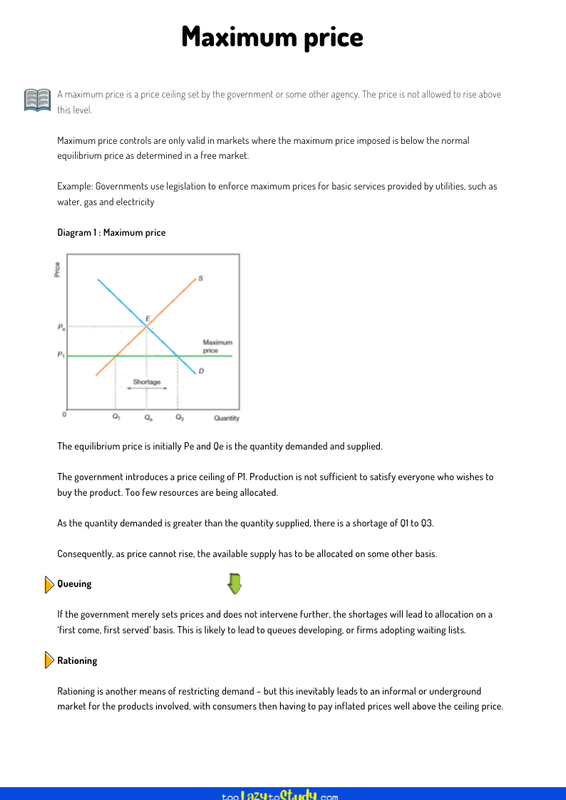

The government introduces a price ceiling of P1. Production is not sufficient to satisfy everyone who wishes to buy the product. Too few resources are being allocated.

As the quantity demanded is greater than the quantity supplied, there is a shortage of Q1 to Q3.

Consequently, as price cannot rise, the available supply has to be allocated on some other basis.

Queuing

If the government merely sets prices and does not intervene further, the shortages will lead to allocation on a ‘first come, first served’ basis. This is likely to lead to queues developing, or firms adopting waiting lists.

Rationing

Rationing is another means of restricting demand – but this inevitably leads to an informal or underground market for the products involved, with consumers then having to pay inflated prices well above the ceiling price.

.png)

Economics notes on

Maximum price

Perfect for A level, GCSEs and O levels!