Overview

Minimum price

A minimum price is a price floor set by the government or some other agency. The price is not allowed to fall below this level

Controls are only valid in markets where the minimum price is set above the normal equilibrium price.

Example: Governments use legislation to enforce minimum prices for:

demerit goods such as tobacco products and alcohol

wages in certain occupations, usually low skilled, to avoid exploitation by employers

certain types of imported goods where domestically produced close substitutes are available

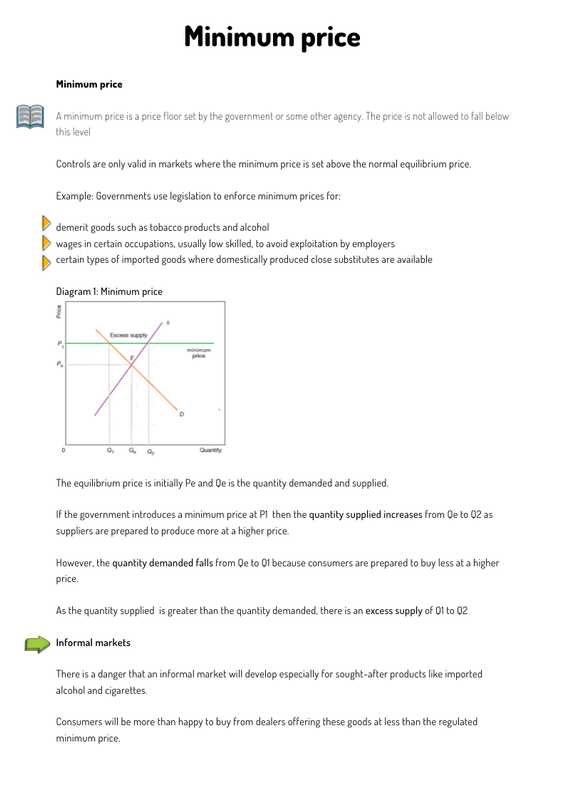

(see Diagram 1: Minimum price)

The equilibrium price is initially Pe and Qe is the quantity demanded and supplied.

If the government introduces a minimum price at P1 then the quantity supplied increases from Qe to Q2 as suppliers are prepared to produce more at a higher price.

However, the quantity demanded falls from Qe to Q1 because consumers are prepared to buy less at a higher price.

As the quantity supplied is greater than the quantity demanded, there is an excess supply of Q1 to Q2

Informal markets

There is a danger that an informal market will develop especially for sought-after products like imported alcohol and cigarettes.

Consumers will be more than happy to buy from dealers offering these goods at less than the regulated minimum price.

.png)

Economics notes on

Minimum price

Perfect for A level, GCSEs and O levels!