Overview

Perfect competition has the following characteristics:

A perfectly competitive market has many firms producing the same (ie homogeneous) goods or services.

Under perfect competition producers and consumers have all the information they require – they have 'perfect knowledge' of the market.

There is complete freedom of entry into and exit from the market.

The price and level of output under perfect competition tends towards the equilibrium point. Producers attempting to sell at a higher price will not sell anything, and producers attempting to sell as a price below equilibrium would obtain 100% market share.

The demand 'curve' is horizontal – it is 'perfectly elastic'.

Examples

In the real world, it's difficult to identify industries that meet all of the 'perfect knowledge' and 'perfect information' criteria.

Some industries, on the other hand, are quite close.

Foreign exchange markets.Here currency is all homogeneous. Traders will also have access to a diverse variety of buyers and sellers. There will be a lot of useful information about pricing comparisons.

It is simple to compare prices while purchasing currencies.

Markets for agricultural products.

In some circumstances, multiple farmers sell identical items to the market, and there are numerous buyers.

It is simple to compare prices at the market.As a result, agricultural markets frequently approach perfect competition.

Is the Internet a real-world example of the perfectly competitive market of the textbooks?

Its claims to be so were quite convincing. For one thing, the vast majority of internet markets appeared to have relatively low entry barriers. Anyone could start an e-retailer of, say, books, compact discs, or downloads.

THE LONG RUN

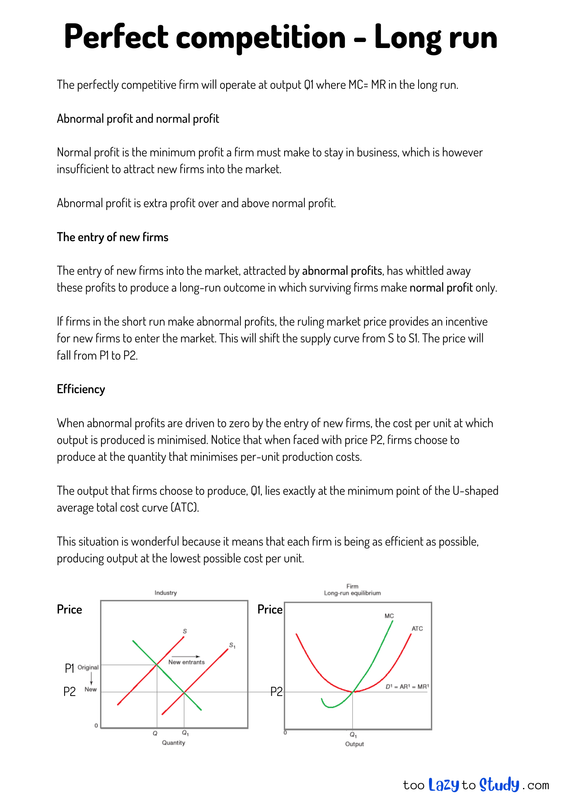

The perfectly competitive firm will operate at output Q1 where MC= MR in the long run.

Abnormal profit and normal profit

Normal profit is the minimum profit a firm must make to stay in business, which is however insufficient to attract new firms into the market.

Abnormal profit is extra profit over and above normal profit.

The entry of new firms

The entry of new firms into the market, attracted by abnormal profits, has whittled away these profits to produce a long-run outcome in which surviving firms make normal profit only.

If firms in the short run make abnormal profits, the ruling market price provides an incentive for new firms to enter the market. This will shift the supply curve from S to S1. The price will fall from P1 to P2.

Efficiency

When abnormal profits are driven to zero by the entry of new firms, the cost per unit at which output is produced is minimised. Notice that when faced with price P2, firms choose to produce at the quantity that minimises per-unit production costs.

The output that firms choose to produce, Q1, lies exactly at the minimum point of the U-shaped average total cost curve (ATC).

This situation is wonderful because it means that each firm is being as efficient as possible, producing output at the lowest possible cost per unit.

.png)

Economics notes on

Perfect competition - Long run

Perfect for A level, GCSEs and O levels!