Overview

Perfect competition has the following characteristics:

A perfectly competitive market has many firms producing the same (ie homogeneous) goods or services.

Under perfect competition producers and consumers have all the information they require – they have 'perfect knowledge' of the market.

There is complete freedom of entry into and exit from the market.

The price and level of output under perfect competition tends towards the equilibrium point. Producers attempting to sell at a higher price will not sell anything, and producers attempting to sell as a price below equilibrium would obtain 100% market share.

The demand 'curve' is horizontal – it is 'perfectly elastic'.

Examples

In the real world, it's difficult to identify industries that meet all of the 'perfect knowledge' and 'perfect information' criteria.

Some industries, on the other hand, are quite close.

Foreign exchange markets.Here currency is all homogeneous. Traders will also have access to a diverse variety of buyers and sellers. There will be a lot of useful information about pricing comparisons.

It is simple to compare prices while purchasing currencies.

Markets for agricultural products.

In some circumstances, multiple farmers sell identical items to the market, and there are numerous buyers.

It is simple to compare prices at the market.As a result, agricultural markets frequently approach perfect competition.

Is the Internet a real-world example of the perfectly competitive market of the textbooks?

Its claims to be so were quite convincing. For one thing, the vast majority of internet markets appeared to have relatively low entry barriers. Anyone could start an e-retailer of, say, books, compact discs, or downloads.

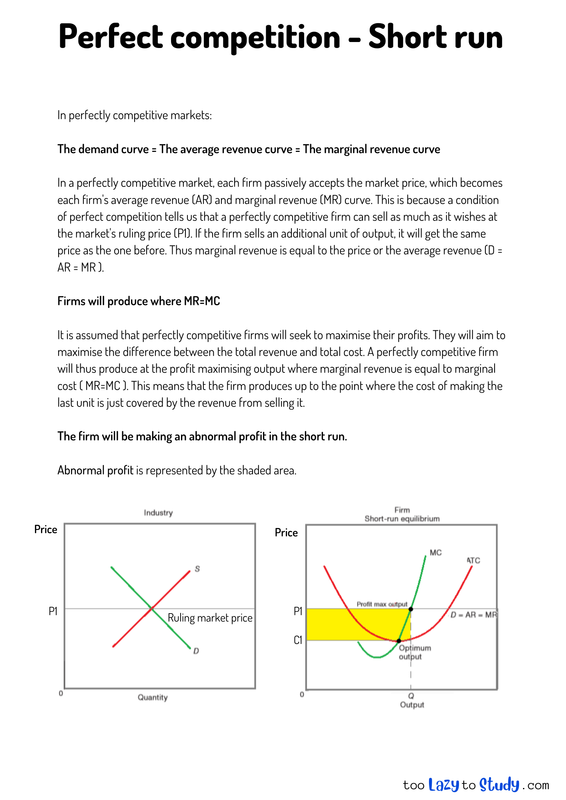

In perfectly competitive markets in the short run:

The demand curve = The average revenue curve = The marginal revenue curve

In a perfectly competitive market, each firm passively accepts the market price, which becomes each firm's average revenue (AR) and marginal revenue (MR) curve. This is because a condition of perfect competition tells us that a perfectly competitive firm can sell as much as it wishes at the market's ruling price (P1). If the firm sells an additional unit of output, it will get the same price as the one before. Thus marginal revenue is equal to the price or the average revenue (D = AR = MR ).

Firms will produce where MR=MC

It is assumed that perfectly competitive firms will seek to maximise their profits. They will aim to maximise the difference between the total revenue and total cost. A perfectly competitive firm will thus produce at the profit maximising output where marginal revenue is equal to marginal cost ( MR=MC ). This means that the firm produces up to the point where the cost of making the last unit is just covered by the revenue from selling it.

The firm will be making an abnormal profit in the short run.

Abnormal profit is represented by the shaded area.

.png)

Economics notes on

Perfect competition - Short run

Perfect for A level, GCSEs and O levels!