Economics explained

Category:

Firm's cost structure

Fixed costs and variable costs

The secret to scoring awesome grades in economics is to have corresponding awesome notes.

A common pitfall for students is to lose themselves in a sea of notes: personal notes, teacher notes, online notes textbooks, etc... This happens when one has too many sources to revise from! Why not solve this problem by having one reliable source of notes? This is where we can help.

What makes TooLazyToStudy notes different?

Our notes:

-

are clear and concise and relevant

-

is set in an engaging template to facilitate memorisation

-

cover all the important topics in the O level, AS level and A level syllabus

-

are editable, feel free to make additions or to rephrase sentences in your own words!

Looking for live explanations of these notes? Enrol now for FREE tuition!

Fixed costs:

A fixed cost is a cost that tends to be unaffected by increases or decreases in the volume of output.

No matter what a business does in any given month, it still has to pay salaried employees and the lease on its office space.

Some firms operate in a situation where the fixed cost represents a large proportion of the total. In this case, it would be wise to produce a large output in order to reduce unit costs and so make the firm more efficient.

Variable costs:

A variable cost is a cost that tends to vary directly with the volume of output.

If you're in the business of creating cotton T-shirts, the more T-shirts you produce, the more cotton fabric you'll need. Raw materials, usage-based utilities, and hourly workers are all variable costs.

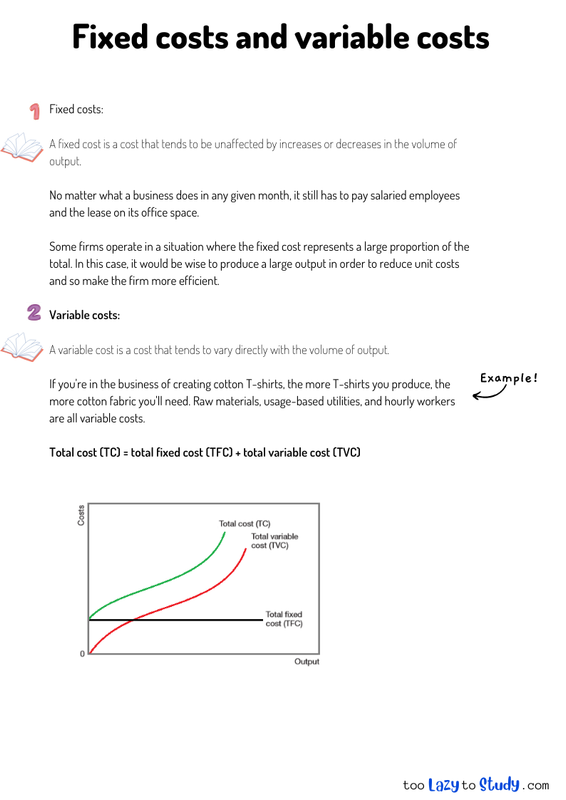

Total cost (TC) = total fixed cost (TFC) + total variable cost (TVC)