Economics explained

Category:

Costs and benefits

Private, external and social costs

The secret to scoring awesome grades in economics is to have corresponding awesome notes.

A common pitfall for students is to lose themselves in a sea of notes: personal notes, teacher notes, online notes textbooks, etc... This happens when one has too many sources to revise from! Why not solve this problem by having one reliable source of notes? This is where we can help.

What makes TooLazyToStudy notes different?

Our notes:

-

are clear and concise and relevant

-

is set in an engaging template to facilitate memorisation

-

cover all the important topics in the O level, AS level and A level syllabus

-

are editable, feel free to make additions or to rephrase sentences in your own words!

Looking for live explanations of these notes? Enrol now for FREE tuition!

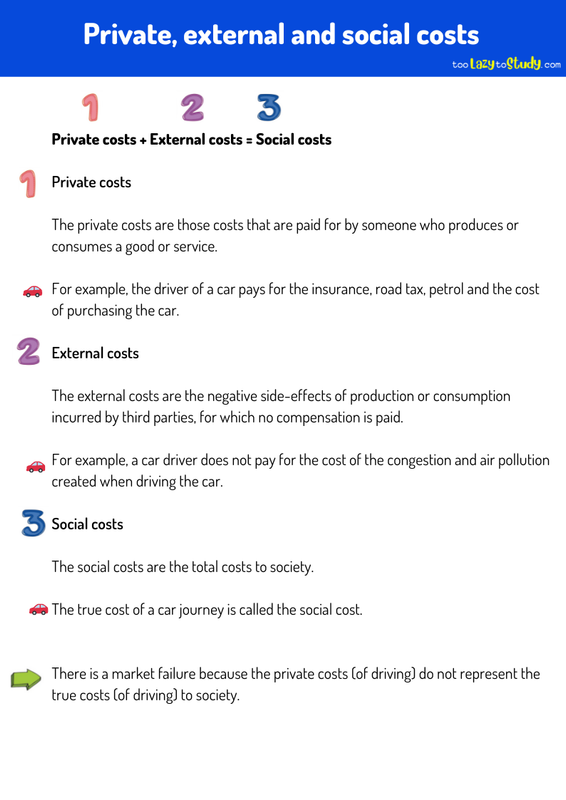

Private costs + External costs = Social costs

Private costs

The private costs are those costs that are paid for by someone who produces or consumes a good or service.

For example, the driver of a car pays for the insurance, road tax, petrol and the cost of purchasing the car.

External costs

The external costs are the negative side-effects of production or consumption incurred by third parties, for which no compensation is paid.

For example, a car driver does not pay for the cost of the congestion and air pollution created when driving the car.

Social costs

The social costs are the total costs to society.

The true cost of a car journey is called the social cost.

There is a market failure because the private costs (of driving) do not represent the true costs (of driving) to society.