Economics explained

Category:

microeconomic policies

Relationship between taxes and income

The secret to scoring awesome grades in economics is to have corresponding awesome notes.

A common pitfall for students is to lose themselves in a sea of notes: personal notes, teacher notes, online notes textbooks, etc... This happens when one has too many sources to revise from! Why not solve this problem by having one reliable source of notes? This is where we can help.

What makes TooLazyToStudy notes different?

Our notes:

-

are clear and concise and relevant

-

is set in an engaging template to facilitate memorisation

-

cover all the important topics in the O level, AS level and A level syllabus

-

are editable, feel free to make additions or to rephrase sentences in your own words!

Looking for live explanations of these notes? Enrol now for FREE tuition!

The relationship between taxation and income varies for different types of tax. Three relationships can be identified:

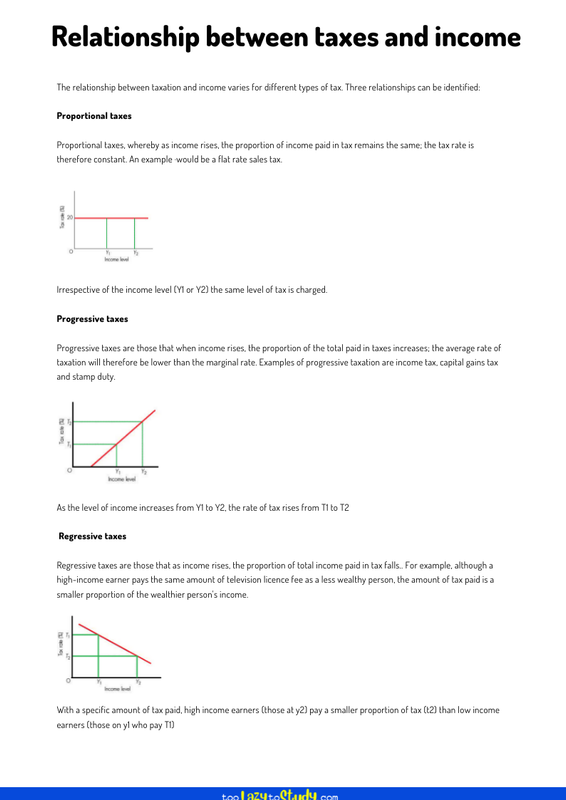

Proportional taxes

Proportional taxes, whereby as income rises, the proportion of income paid in tax remains the same; the tax rate is therefore constant. An example ·would be a flat rate sales tax.

Irrespective of the income level (Y1 or Y2) the same level of tax is charged.

Progressive taxes

Progressive taxes are those that when income rises, the proportion of the total paid in taxes increases; the average rate of taxation will therefore be lower than the marginal rate. Examples of progressive taxation are income tax, capital gains tax and stamp duty.

As the level of income increases from Y1 to Y2, the rate of tax rises from T1 to T2

Regressive taxes

Regressive taxes are those that as income rises, the proportion of total income paid in tax falls.. For example, although a high-income earner pays the same amount of television licence fee as a less wealthy person, the amount of tax paid is a smaller proportion of the wealthier person's income.

With a specific amount of tax paid, high income earners (those at y2) pay a smaller proportion of tax (t2) than low income earners (those on y1 who pay T1)