Economics explained

Category:

Efficiency

The free market and efficiency

The secret to scoring awesome grades in economics is to have corresponding awesome notes.

A common pitfall for students is to lose themselves in a sea of notes: personal notes, teacher notes, online notes textbooks, etc... This happens when one has too many sources to revise from! Why not solve this problem by having one reliable source of notes? This is where we can help.

What makes TooLazyToStudy notes different?

Our notes:

-

are clear and concise and relevant

-

is set in an engaging template to facilitate memorisation

-

cover all the important topics in the O level, AS level and A level syllabus

-

are editable, feel free to make additions or to rephrase sentences in your own words!

Looking for live explanations of these notes? Enrol now for FREE tuition!

Firms in perfect competition in a free market are able to achieve both productive and allocative efficiency.

In perfect competition, there are very many firms competing. Each firm is so small relative to the whole industry that it has no power to influence the price. It is a price taker.

Productive efficiency occurs at the lowest point on the firm’s average costs curve.

This means that the maximum number of goods and services are produced with a given amount of inputs.

Allocative efficiency will occur at an output level where price equals the marginal cost of production.

At this point, there is no wastage and both producers and consumers are satisfied with what is produced. This is because the price that consumers are willing to pay is equivalent to the marginal benefit that they get. Therefore the optimal distribution is achieved when the marginal benefit of the good equals the marginal cost.

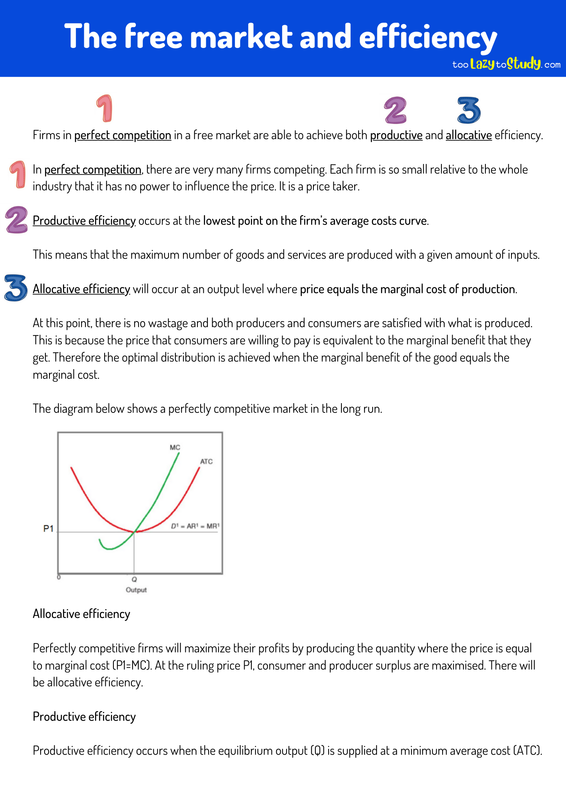

The diagram below shows a perfectly competitive market in the long run.

Allocative efficiency

Perfectly competitive firms will maximize their profits by producing the quantity where the price is equal to marginal cost (P1=MC). At the ruling price P1, consumer and producer surplus are maximised. There will be allocative efficiency.

Productive efficiency

Productive efficiency occurs when the equilibrium output (Q) is supplied at a minimum average cost (ATC).